Introduction

The Securities and Exchange Commission (the “SEC” or the “Commission“) recently finalized sweeping new rules for private fund advisers (the “Final Rules”) under the Investment Advisers Act of 1940.[1] According to the SEC, the Final Rules are designed to increase the SEC’s oversight, bolster the regulation of private fund advisers, and update the existing compliance rule that applies to all investment advisers.

With the Final Rules now projected to become effective in mid-November 2023, private fund advisers would be wise to become familiar with the rule changes. The changes will considerably expand the SEC’s oversight of private fund advisers and impose onerous compliance burdens on them. Advisers to private funds should start (or continue to) make efforts to fully understand their upcoming compliance obligations, identify critical next steps they will need to take to comply under this changing regulatory regime, and appreciate the key considerations and potential implications associated with these upcoming regulatory changes.

The recent changes are facing ongoing legal challenges in federal court,[2] but private fund advisers would still be well-advised to proceed with the expectation that enactment remains likely in the short-term. As private fund advisers consider next steps and best practices to comply with the Final Rules, this alert provides a streamlined overview of these significant changes and their potential implications for both private fund advisers and investors.

Principal Regulatory Highlights:

- Greater Mandated Information Rights for Investors

- Strengthened Compliance and Disclosure Standards and Audit and Quarterly Statement Obligations for Advisers

- Regulations on Use of Side Letters and Preferential Treatment

Key Amendments At A Glance

- Consistent with the continued trend of the SEC’s emphasis on enhancing disclosures and transparency to investors, the new rules and amendments are designed to protect private fund investors by increasing transparency, competition, and efficiency in the private funds market.

- Many of the most onerous and contentious provisions in the February 9, 2022[3] rule proposal were abandoned or significantly modified in the Final Rules.

- Even private fund advisers that are not required to be registered with the SEC should take note that certain requirements under the Final Rules apply universally to all private fund advisers, irrespective of their registration status with the SEC.

Key Changes for Registered Private Fund Advisers:

- Quarterly Statements on Performance, Fees and Expenses:[4] Fund Advisers must now provide investors with quarterly statements that include details such as fund fees, expenses, and performance, among other measures aimed at bolstering transparency and mitigating conflicts.

- Mandatory Annual Audits: Every private fund advised by a registered adviser must now have an annual financial statement audit. This audit must be executed by an independent public accountant and subsequently shared with investors.

- Adviser-Led Secondary Transactions: If advisers are offering current fund investors an option to sell or swap their interests, they need to validate their decision with a fairness or valuation opinion. Further, any significant relationship with the entity giving this opinion must be disclosed.

- Books and Records: Registered private fund advisers are now required to maintain and retain specific records associated with the new rules, including those related to quarterly statements, annual audits, disclosures about restricted activities, and preferential treatment. This amendment is aimed at strengthening the Commission’s capability to assess an adviser’s compliance to these rules.

All Private Fund Advisers:

Restricted Activities Rule: The reforms aim to address specific conflicts of interest and establish a new rule that ensures investor protection and upholds public interest. Accordingly, all private fund advisers are prohibited from:

- Regulatory Expenses: Advisers can’t shift expenses related to investigations by regulatory authorities onto a private fund. However, If these expenses are clearly communicated in writing to investors within a 45-day period after the end of the fiscal quarter when they’re incurred, the shifting is acceptable.

- Investigation Sanctions: If there’s a sanction due to a violation of the Investment Advisers Act of 1940 or its related rules, advisers cannot transfer the investigation costs to the private fund.

- Adviser Clawbacks: If an adviser adjusts their clawback due to actual, potential, or hypothetical taxes, they must be transparent about it. This means offering a clear written notice, detailing the aggregate dollar amounts before and after the adjustments, within 45 days of the end of the fiscal quarter in which the clawback happens.

- Non-Pro Rata Fee Allocations: Fees and expenses related to a private fund investment (held by multiple funds), if allocated on a non-pro rata basis, must be justified as fair. Advisers should provide a written description justifying this fairness.

- Borrowing and Lending: Borrowing assets or obtaining credit from a private fund is permitted only when the material terms are clearly communicated in writing to the fund’s investors and written consent is obtained. The SEC states in the Adopting Release that this prohibition will not prohibit a private fund adviser from borrowing directly from individual investors outside of the fund.

Preferential Treatment Rule: These reforms are designed to counteract the adverse impacts of certain types of preferential treatment on other investors. All private fund advisers:

- Must not offer preferential terms connected to redemptions or access to essential information if these terms might negatively affect other investors.

- Are required to ensure transparency. Any special terms or treatments must be disclosed to both current and prospective investors. As long as all investors are kept informed, funds can continue to provide these preferential conditions.

- Must not provide any preferential terms granting special redemption rights or offering enhanced access to essential information unless every investor is offered these rights.

Legacy Status: The Commission has introduced “legacy status” provisions, which are designed to address some burdens associated with revisiting pre-existing agreements. The legacy status provisions grant legacy status to the prohibitive aspects of the Preferential Treatment Rule and elements of the Restricted Activities Rule that requires investor consent. These provisions pertain to governing agreements that were entered into before the compliance date if the applicable rules would require the parties to modify existing agreements.

Exemptions and Special Cases:

- Registration Status: While the quarterly statement, private fund audit, and adviser-led secondaries rules are exclusive to SEC-registered private fund advisers, the restricted activities and preferential treatment rules encompass all private fund advisers.

- Offshore Advisers and Funds: Offshore advisers, even if they’re registered with the SEC, get a pass when it comes to offshore funds. This interpretation applies regardless of whether such non-U.S. private funds have U.S. investors.

- Securitized Asset Funds: The SEC has carved out an exception for these funds, which generally encompass entities like collateralized loan obligations.

Specific Adviser Regulations

Historically, private funds have attracted early stage or substantial investors by offering them special terms. These preferential terms, often contained in “side letters,” serve dual purposes: they help funds grow their asset base while simultaneously enhancing their credibility in the eyes of potential new investors.

The SEC’s changes under the Final Rules have slightly shifted their approach toward these side letters. Instead of a strict regulation, the Final Rules establish that private fund advisers cannot offer any investor preferential terms related to redemptions or access to information if such terms would be detrimental to other investors. There are, of course, some exceptions to this. For other kinds of preferential treatment, the rules prioritize transparency. Advisers will have to disclose these special terms to all current and potential investors. Essentially, as long as all investors are informed, funds can continue granting these favorable conditions. Furthermore, any preferential terms that offer special rights related to redemptions or provide enhanced access to information must be made available to every investor.

As a result of the preferential treatment rule, private fund advisers will be required to disclose to all fund investors any “side letters” or other preferential rights granted to any fund investor. However, the rule requires disclosure of preferential treatment, not only the granting of preferential treatment rights. Accordingly, any practice which treats fund investors differently should be scrutinized to determine whether such treatment should be disclosed to all fund investors.

Recognizing the complexities of revisiting existing agreements, the Commission has provided “legacy status” provisions designed to relieve at least some level of burden by grandfathering certain portions of the Restricted Activities Rule and Preferential Treatment Rule described in this alert with respect to preexisting contractual arrangements. However, as noted elsewhere, this grandfathering clause does not allow investment advisers to charge for fees or expenses related to an investigation that results or has resulted in a court or governmental authority imposing sanctions for violations of the Advisers Act or the rules promulgated thereunder.

Adviser Preparedness and Next Steps

In light of the new rules, it’s an important time for advisers. They must not only become familiar with the complexities of these regulations but also be proactive in strategizing to adopt any necessary changes to their compliance programs. Since the Final Rules have varying compliance dates, advisers would benefit from crafting a comprehensive timeline, detailing the implementation phases for each regulation. Advisers should particularly focus on:

- Emphasis on Transparency: Advisers should anticipate a transition phase where they adapt to clearer communication standards.

- Operational Adjustments: These new regulations might mean that advisers will undergo operational changes, including more stringent report data collection and potentially collaborating with additional service providers.

- Regular Review and Updates: Advisers are encouraged to review their current practices, ensure they align with the new disclosure mandates, and prepare for any additional data collection or audits.

Conclusion

These new rules and amendments can have a material impact on private fund advisers, regardless of whether they are SEC-registered, and could significantly increase the compliance costs for private fund advisers. Moreover, these rules and amendments change long-standing, negotiated market practices applicable to private fund advisers.

ADDENDUM

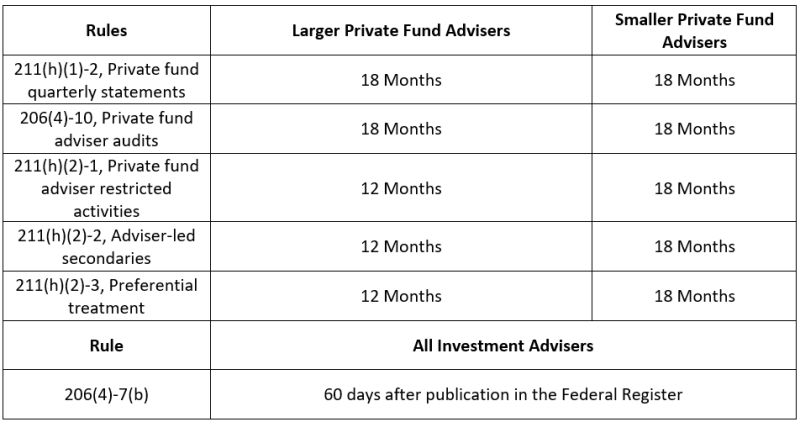

Compliance Dates

The Final Rules will come into effect November 13, 2023 (referred to as the “Effective Date”). The specific compliance dates for different rules vary based on the type of provision and the size of the private fund adviser. Here is a detailed breakdown:

- Immediate Compliance: The amended Compliance Rule has a compliance date set just 60 days after the Effective Date.

- Private Fund Adviser Assets:

- For advisers with $1.5 billion or more in private fund assets:

- The compliance date for adviser-led secondaries, preferential treatment, and restricted activities rules will be 12 months after the Effective Date.

- For advisers with less than $1.5 billion in private fund assets:

- The compliance date for these provisions will be 18 months after the Effective Date.

- For advisers with $1.5 billion or more in private fund assets:

Detailed Compliance Timeline:

[1] Private Fund Advisers; Documentation of Registered Investment Adviser Compliance Reviews, SEC Release No. IA-6383 (Aug. 23, 2023) (the “Release”). See also SEC Fact Sheet: Private Fund Adviser Reforms: Final Rules (Aug. 23, 2023), available at https://www.sec.gov/files/ia-6383-factsheet.pdf.

[2] On September 1, 2023, the National Association of Private Fund Managers, in conjunction with the Alternative Investment Management Association Limited (AIMA) and four other business trade associations, filed suit in the US Court of Appeals for the Fifth Circuit. Their petition seeks to invalidate the final Private Fund Advisers Rules. NA of Private Fund Managers v. SEC, 23-60471, (5th Cir.)

[3] Private Fund Advisers; Documentation of Registered Investment Adviser Compliance Reviews, SEC Release No. IA-5955 (Feb. 9, 2022).

[4] While not discussed in the text of the Rules themselves, the SEC has indicated that it might someday consider extending the Quarterly Statement Rule and the Private Fund Audit Rule to Exempt Reporting Advisers (“ERAs”). However, the SEC made clear that it would need considerably more input prior to proposing application to ERAs and is thus not a concern at this time.