Any United States company that has at least one non-U.S. investor owning at least 10% of its voting equity (“U.S. Affiliates”) must file an appropriate report with the Bureau of Economic Analysis (“BEA”) of the U.S. Department of Commerce by May 31, 2023, for its Benchmark Survey of Foreign Direct Investment in the United States. This Alert will provide a summary of this important, and sometimes overlooked, disclosure obligation.

The BEA conducts the Benchmark Survey of Foreign Direct Investment in the United States once every five years, for years ending in 2 and 7. The current Survey applies to 2022. The 5-year survey is one of many surveys required under the International Investment and Trade in Services Survey Act of 1976. (Others include the BE-15 Annual Survey [similar, slightly less comprehensive survey for years other than years ending in 2 and 7], transactionally driven BE-13 New FDI Survey [for FDI -foreign acquisitions and investments] and BE-605 Quarterly Survey.)

BEA uses the collected information to analyze foreign investment activity in the U.S. The information submitted is required to be kept confidential. One cannot, for example, enter any personally identifiable information on the filings. Anonymized data is aggregated for publicly available financial reports. The Act is a relatively obscure piece of legislation and, as a result, the reporting requirements it imposes are easily and often overlooked.

U.S. Affiliates are required to report using one of the first three versions of Form BE-12 (discussed below) by May 31, 2023. The deadline is June 30, 2023 for entities that use BEA’s internet portal. If the U.S. company has foreign owner(s) but is not a U.S. Affiliate – for example, because the foreign investor does not hold at least 10% of voting equity – the company will not be required to report unless requested by the BEA.

The version of Form BE-12 a particular company must use depends upon its financial condition (assets, sales or net income) and foreign voting percentage (majority – greater than 50% and minority – 50% or less).

Below, we will set forth specific information about the disclosure requirements for the survey.

Who must report.

A BE-12 report is required for each U.S. Affiliate (except certain private funds) that is, for each U.S. business enterprise (any organization, association, branch, or venture that exists for profit making purposes or to otherwise secure economic advantage, and ownership of any real estate that is not held for personal use) in which a foreign person (foreign parent) owned or controlled, directly or indirectly, 10 percent or more of the voting securities at the end of the business enterprise’s fiscal year ending in 2022.

Forms to be filed.

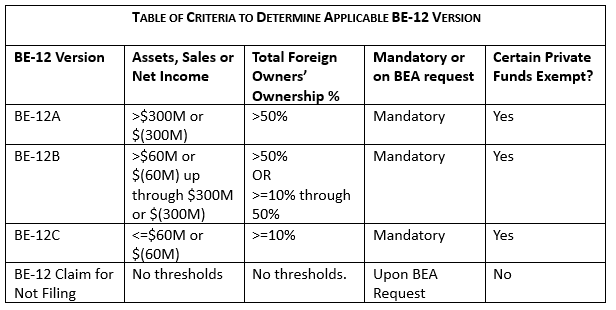

Form BE-12A must be completed by a U.S. Affiliate that was majority-owned by one or more foreign parents if, on a fully consolidated basis, (or, in the case of real estate investment, on an aggregated basis) any one of total assets, sales or net income for the U.S. affiliate (not just the foreign parent’s share) was greater than $300 million (positive or negative) at the end of, or for, its fiscal year ending in 2022. For purposes of this survey, a “majority-owned” U.S. Affiliate is one in which the combined direct and indirect ownership interest of all foreign parents of the U.S. affiliate exceeds 50 percent.

Form BE-12B must be completed by a majority-owned U.S. Affiliate if, on a fully consolidated basis, (or, in the case of real estate investment, on an aggregated basis), any one of total assets, sales or net income (not just the foreign parent’s share), was greater than $60 million (positive or negative) but none of these items was greater than $300 million (positive or negative) at the end of, or for, its fiscal year ending in 2022.

This form must also be used by a minority-owned U.S. Affiliate (one in which the combined direct and indirect ownership interest of all foreign parents of the U.S. affiliate is 50 percent or less) if, on a fully consolidated basis, (or, in the case of real estate investment, on an aggregated basis) any one of total assets, sales or net income (not just the foreign parent’s share), was greater than $60 million (positive or negative) at the end of, or for, its fiscal year ending in 2022.

Form BE-12C must be completed by a U.S. affiliate if, on a fully consolidated basis, (or, in the case of real estate investment, on an aggregated basis), none of total assets, sales or net income for a U.S. affiliate (not just the foreign parent’s share), was greater than $60 million (positive or negative) at the end of, or for, its fiscal year ending in 2022.

BE-12 Claim for Not Filing. Any U.S. company that is contacted by BEA concerning the BE-12 survey, but is not subject to the reporting requirements, must file a BE-12 Claim for Not Filing.

No Form BE-12 Required. Generally, if a company is not required to file Forms BE-12 A, B or C and if the BEA does not request the company to file Form BE-12 Claim for Not Filing, the Company is not required to file any Form BE-12.

Due date. Forms BE-12 are due not later than May 31, 2023 (or by June 30, 2023 for reporting companies that use BEA’s eFile system).

Penalties. Civil penalties range from $2,500 to $25,000 (and injunctive relief compelling compliance). Criminal penalties (including for officers and directors) for willful failure to file are up to $10,000 and up to 1 year in prison.

Extensive Reporting. The BE-12 forms are complex and call for the reporting of extensive information to enable BEA to publish comprehensive statistics on the United States economy.

M&A Due Diligence. Compliance with this little-known Act should be added to the Due Diligence Checklist for cross-border M&A transactions involving U.S. affiliated entities of foreign persons.

Practical Application; Thresholds. In determining the appropriate Form BE-12 version, the Form BE-12 regulations and instructions provide various criteria or “thresholds,” the second level of which is summarized in the table below. The first level mandatory filing threshold is that the U.S. company fall within the “Affiliate” terms set forth above, namely, a company “in which a foreign person (foreign parent) owned or controlled, directly or indirectly, 10 percent or more of the voting securities.” In other words, the first threshold for mandatory (as distinguished from BEA-requested) filings is generally only crossed under circumstances where a minimum of one foreign investor owns or controls at least 10 percent of the voting equity. There appears to be no first level threshold (or other thresholds) for filing a Form BE-12 Claim for Not Filing if requested by BEA.

Further Information

This Alert is only a summary. If you have questions concerning how Form BE-12 and its versions may apply to your company, please contact Russ Hansen.